Understanding above-the-line versus itemized deductions can save you thousands on your tax bill. Above-the-line deductions reduce your adjusted gross income (AGI) before you calculate taxes, while itemized deductions compete with the standard deduction to lower your taxable income. Every taxpayer qualifies for above-the-line deductions, but only those with expenses exceeding the standard deduction benefit from itemizing. Knowing which deductions to claim—and when—puts more money in your pocket.

Quick Facts: Tax Deductions Comparison

| Category | Above-the-Line | Itemized Deductions |

|---|---|---|

| Other Name | Adjustments to income | Below-the-line deductions |

| When Applied | Before calculating AGI | After calculating AGI |

| Who Benefits | Everyone who qualifies | Those exceeding standard deduction |

| 2026 Standard Deduction | N/A | $16,100 (single), $32,200 (married) |

| AGI Impact | Lowers AGI | No AGI impact |

| Common Examples | HSA, IRA, student loan interest | Mortgage interest, property taxes |

| Where Reported | Schedule 1, Part II | Schedule A |

| Must Choose | No—claim all you qualify for | Yes—standard vs itemized |

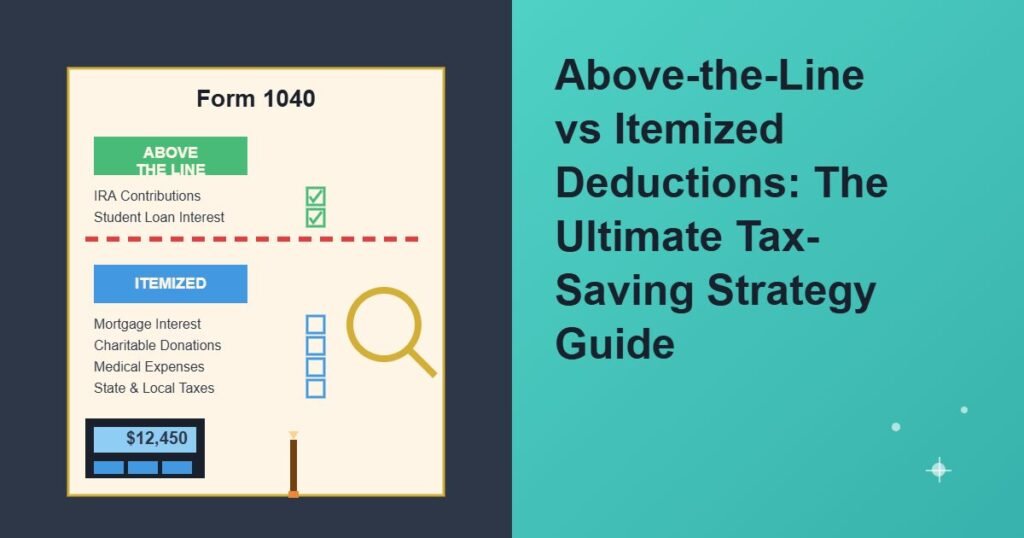

What Are Above-the-Line Deductions?

Above-the-line deductions reduce your gross income before you calculate your adjusted gross income (AGI). These deductions appear on Schedule 1, Part II of Form 1040, and they sit “above the line” that shows your AGI.

Your AGI matters because it determines eligibility for other tax benefits. Lower AGI means you qualify for more credits, deductions, and government programs. Above-the-line deductions give you this advantage automatically.

You can claim above-the-line deductions whether you take the standard deduction or itemize. This makes them valuable for every taxpayer. You don’t choose between above-the-line deductions and other deductions—you stack them on top of everything else.

Common above-the-line deductions include:

- Self-employment tax deduction (50% of SE tax paid)

- Health Savings Account (HSA) contributions

- Health insurance premiums for self-employed

- Traditional IRA contributions

- Student loan interest (up to $2,500)

- Educator expenses (up to $300)

- Alimony payments (for divorces finalized before 2019)

- Penalty on early withdrawal of savings

A freelancer who earns $80,000 and contributes $7,000 to a traditional IRA reduces their AGI to $73,000. This lower AGI can qualify them for credits they’d miss at $80,000.

What Are Itemized Deductions?

Itemized deductions reduce your taxable income after you calculate your AGI. These deductions appear on Schedule A of Form 1040, and they compete directly with the standard deduction.

You must choose between taking the standard deduction or itemizing your deductions. You cannot do both. Most taxpayers take the standard deduction because it exceeds their itemized deductions.

The standard deduction amounts for 2026 are:

- Single filers: $16,100

- Married filing jointly: $32,200

- Head of household: $24,150

- Married filing separately: $16,100

You should itemize only when your total itemized deductions exceed the standard deduction for your filing status. Running the numbers both ways shows which option saves you more money.

Common itemized deductions include:

- Mortgage interest (on loans up to $750,000)

- State and local taxes—SALT (capped at $10,000)

- Property taxes (included in SALT cap)

- Charitable contributions (up to 60% of AGI for cash)

- Medical expenses (exceeding 7.5% of AGI)

- Casualty and theft losses (from federally declared disasters)

A married couple with $25,000 in mortgage interest, $10,000 in SALT, and $5,000 in charitable donations totals $40,000 in itemized deductions. This exceeds their $32,200 standard deduction, saving them an extra $7,800 in taxable income.

Key Differences Between Above-the-Line and Itemized Deductions

| Factor | Above-the-Line | Itemized Deductions |

|---|---|---|

| Timing | Reduces income before AGI | Reduces income after AGI |

| AGI Impact | Lowers your AGI | Doesn’t affect AGI |

| Eligibility | Based on specific actions | Must exceed standard deduction |

| Choice Required | No—claim all that apply | Yes—itemize or standard |

| Benefit Threshold | $1 saved equals tax benefit | Must exceed $16,100+ to benefit |

| Other Benefits | Opens doors to credits/programs | Only reduces taxable income |

| Recordkeeping | Moderate documentation | Extensive receipts required |

| Who Benefits Most | Self-employed, savers, students | Homeowners, high earners |

Why Your AGI Matters

Your adjusted gross income determines whether you qualify for dozens of tax benefits and government programs. Lower AGI opens doors that higher AGI closes.

Programs and benefits tied to AGI include:

- Premium tax credits for health insurance

- Child Tax Credit eligibility

- Earned Income Tax Credit (EITC)

- American Opportunity Tax Credit

- Lifetime Learning Credit

- Deductible IRA contributions

- Roth IRA contribution limits

- Student loan interest deduction

- Medicare premium surcharges

- Net Investment Income Tax threshold

A single filer earning $85,000 who contributes $7,000 to an HSA and $6,500 to a traditional IRA drops their AGI to $71,500. This $13,500 reduction might qualify them for education credits or reduce their student loan payment under income-driven repayment plans.

Itemized deductions don’t touch your AGI. They reduce taxable income, which saves you money on taxes. But they don’t qualify you for programs tied to AGI thresholds.

People also love to read this: How to Lower Car Insurance After DUI or Accident

Common Above-the-Line Deductions Explained

Self-Employment Tax Deduction

Self-employed individuals pay both the employer and employee portions of Social Security and Medicare taxes—a total of 15.3%. The IRS lets you deduct 50% of your self-employment tax as an above-the-line deduction.

A consultant who earns $100,000 pays approximately $15,300 in self-employment tax. They can deduct $7,650 above the line, reducing their AGI to $92,350.

Health Savings Account (HSA) Contributions

Contributing to an HSA gives you a triple tax advantage. You deduct contributions above the line, money grows tax-free, and withdrawals for medical expenses are tax-free.

For 2026, contribution limits are:

- Individual coverage: $4,300

- Family coverage: $8,550

- Catch-up (age 55+): Additional $1,000

You must have a high-deductible health plan (HDHP) to qualify. The 2026 HDHP minimum deductibles are $1,650 for individual coverage and $3,300 for family coverage.

Traditional IRA Contributions

Traditional IRA contributions reduce your AGI dollar-for-dollar. The 2026 contribution limit is $7,000 ($8,000 if age 50 or older).

Income limits phase out this deduction if you’re covered by a workplace retirement plan:

- Single filers: Begins phasing out at $79,000

- Married filing jointly: Begins phasing out at $126,000

You can still contribute if your income exceeds these limits, but you won’t get the above-the-line deduction.

Student Loan Interest Deduction

You can deduct up to $2,500 of student loan interest paid during the year. This deduction phases out for higher earners:

- Single filers: Phases out between $80,000 and $95,000

- Married filing jointly: Phases out between $165,000 and $195,000

A recent graduate paying $3,000 in student loan interest who earns $70,000 can deduct the full $2,500, reducing their AGI to $67,500.

Health Insurance Premiums (Self-Employed)

Self-employed individuals can deduct health insurance premiums for themselves, their spouse, and their dependents. This includes medical, dental, and long-term care insurance.

A self-employed photographer paying $12,000 annually for family health insurance deducts the full amount above the line. This reduces taxable income and self-employment tax.

Common Itemized Deductions Explained

Mortgage Interest Deduction

You can deduct interest paid on mortgages up to $750,000 ($375,000 if married filing separately). This limit applies to loans taken after December 15, 2017. Older mortgages follow a $1 million limit.

A homeowner with a $600,000 mortgage at 6.5% interest pays roughly $39,000 in interest annually. They can deduct the full amount if they itemize.

State and Local Tax (SALT) Deduction

The SALT deduction covers state and local income taxes, sales taxes, and property taxes. The IRS caps this deduction at $10,000 ($5,000 if married filing separately).

High-tax states like California, New York, and New Jersey see many taxpayers hit this cap. A homeowner paying $8,000 in property taxes and $5,000 in state income taxes can only deduct $10,000 total.

Charitable Contributions

Cash donations to qualified charities are deductible up to 60% of your AGI. Non-cash donations (clothing, vehicles, property) have different limits and require documentation.

A taxpayer earning $100,000 who donates $20,000 to qualified charities can deduct the full $20,000 if they itemize. This requires receipts for donations over $250.

Medical Expenses

You can deduct medical and dental expenses exceeding 7.5% of your AGI. This high threshold means few taxpayers benefit unless they face major medical bills.

A single filer with $80,000 AGI needs more than $6,000 in medical expenses to claim any deduction. If they spent $12,000 on medical care, they can deduct $6,000 ($12,000 – $6,000 threshold).

Standard Deduction vs Itemizing: Which Wins?

About 90% of taxpayers take the standard deduction because it exceeds their itemized deductions. The 2017 Tax Cuts and Jobs Act nearly doubled the standard deduction, making itemizing less common.

Calculate your total itemized deductions before deciding. Add up mortgage interest, SALT, charitable contributions, and medical expenses. Compare this total to your standard deduction.

Take the standard deduction if:

- You own no home or your mortgage is paid off

- You live in a low-tax state

- Your charitable giving is modest

- You have minimal medical expenses

- Your total itemized deductions fall below $16,100 (single) or $32,200 (married)

Itemize if:

- You pay substantial mortgage interest

- You live in high-tax states like California or New York

- You make large charitable contributions

- You faced major medical expenses

- Your total itemized deductions exceed the standard deduction

A homeowner in Texas with a $400,000 mortgage might benefit from itemizing. Their mortgage interest ($26,000), property taxes ($8,000 capped), and charitable giving ($5,000) totals $39,000—well above the $32,200 standard deduction for married couples.

Tax Planning Strategies to Maximize Deductions

Front-Load Itemized Deductions

“Bunching” deductions means concentrating itemized expenses into one tax year. You itemize in high-expense years and take the standard deduction in low-expense years.

Make two years of charitable donations in one year. Schedule elective medical procedures together. Prepay property taxes if your state allows it. This strategy pushes itemized deductions above the standard deduction threshold.

Max Out Above-the-Line Deductions

Contribute the maximum to HSAs, IRAs, and other accounts offering above-the-line deductions. These reduce your AGI and stack on top of your standard deduction or itemized deductions.

A self-employed single filer contributing $4,300 to an HSA and $7,000 to an IRA reduces their AGI by $11,300. They still claim the $16,100 standard deduction, reducing taxable income by $27,400 total.

Track All Deductible Expenses

Keep receipts for charitable donations, medical expenses, and property taxes throughout the year. Calculate your itemized deductions quarterly to see if you’ll exceed the standard deduction.

Use apps like Expensify, QuickBooks, or simple spreadsheets to track deductible expenses. This preparation saves time during tax season and ensures you don’t miss valuable deductions.

Consider Timing

Delay or accelerate deductible expenses based on your tax situation. If you’re close to the itemizing threshold in December, prepay January property taxes or make year-end charitable donations to push over the limit.

Your income matters too. If you expect higher income next year, accelerate deductions into the current year when they provide more value.

People also love to read this: Teen Driver Insurance Costs and Discount Strategies

Special Considerations for Different Taxpayers

Self-Employed Individuals

Self-employed taxpayers benefit heavily from above-the-line deductions. They can deduct:

- 50% of self-employment tax

- Health insurance premiums

- HSA contributions

- Retirement plan contributions (SEP IRA, Solo 401(k))

- Home office expenses (on Schedule C, not as itemized deduction)

These deductions reduce both income tax and self-employment tax, creating double savings.

Homeowners

Homeowners typically benefit from itemizing during their first 10-15 years of mortgage ownership when interest payments are highest. As the mortgage ages, principal payments increase while interest decreases.

Calculate each year whether itemizing or the standard deduction saves more money. Your break-even point shifts as your mortgage balance drops.

Seniors (Age 65+)

Taxpayers 65 and older qualify for an additional standard deduction:

- Single or head of household: Additional $2,050

- Married filing jointly: Additional $1,650 per qualifying spouse

The 2026 standard deduction for a married couple both age 65+ is $35,500 ($32,200 + $1,650 + $1,650). This makes itemizing harder to justify unless expenses are substantial.

Seniors may also qualify for the new $6,000 bonus deduction (phasing out above $75,000 single, $150,000 married). This temporary benefit runs through 2028.

High-Income Earners

High earners face additional considerations:

- Many above-the-line deductions phase out at higher incomes

- SALT cap hurts those in high-tax states

- Alternative Minimum Tax (AMT) may limit benefits

- Net Investment Income Tax (3.8%) applies above certain thresholds

Consult a tax professional to navigate complex high-income tax planning strategies.

Frequently Asked Questions

Can I claim both above-the-line deductions and itemized deductions?

Yes, but you choose between itemizing and the standard deduction. Above-the-line deductions reduce your AGI first. Then you either itemize or take the standard deduction to reduce taxable income further. Above-the-line deductions stack on top of whichever option you choose for below-the-line deductions.

What happens if my itemized deductions equal exactly the standard deduction?

Take the standard deduction. It requires zero documentation and no Schedule A filing. If both options save the same amount of tax, choose the simpler path. The standard deduction carries less audit risk and takes seconds to claim on your tax return.

Do above-the-line deductions reduce my self-employment tax?

Some do, most don’t. The self-employment tax deduction reduces income tax but not SE tax (it’s already calculated). HSA contributions made through your business reduce both income tax and SE tax. IRA contributions and student loan interest deductions only reduce income tax, not SE tax.

Should I itemize if I’m close to the standard deduction amount?

Run the numbers carefully. If your itemized deductions exceed the standard deduction by $500 or more, itemize. Smaller differences might not justify the extra recordkeeping and Schedule A filing requirements. Consider the time value of your effort and potential audit risk.

How do above-the-line deductions affect my state taxes?

It depends on your state. Most states use federal AGI as their starting point, so above-the-line deductions reduce both federal and state taxes. Some states add back certain federal deductions or have their own rules. Check your state’s tax forms or consult a local tax professional.

Final Thoughts

Understanding above-the-line versus itemized deductions helps you keep more of your hard-earned money. Above-the-line deductions reduce your AGI, opening doors to additional tax benefits and programs. Itemized deductions compete with the standard deduction to lower your taxable income.

Most taxpayers benefit from maximizing above-the-line deductions while taking the standard deduction. Homeowners in high-tax states with large mortgages often benefit from itemizing. Calculate both options annually to find your best strategy.

Track deductible expenses throughout the year using apps or spreadsheets. This organization saves time during tax season and ensures you claim every deduction you deserve. Front-load expenses in years when itemizing makes sense, and spread them out when taking the standard deduction saves more.

Consider working with a tax professional if your situation involves self-employment income, rental properties, significant investments, or complex itemized deductions. Professional guidance can identify opportunities you might miss and ensure you’re using the right strategy for your circumstances.

The tax code rewards those who understand it. Above-the-line and itemized deductions represent powerful tools for reducing your tax bill—use them wisely to keep more money working for you instead of going to the IRS.